How often have we come across a family suffering financially even after working throughout their whole lives? Most people earn enough to live their lives comfortably but the lack of planning their financial goals leads to spending a major part of their life struggling with monetory issues. So, every one of us needs to do financial planning in order to meet our needs as and when they arise.

While there are some needs that will arise for certain, there are also needs that arise without our prior knowledge. So, we need to plan both for certain needs and uncertain or accidental needs.

| Table of Contents |

|---|

| What is the best time to start saving? |

| How much should you save each month for achieving Financial Goals? |

| Where to put your money? |

| Tips for Financial Goals |

What is the best time to start saving?

Now, typically a person starts earning around the age of 25. The question arises when she/he should start saving for future. To answer this question and to justify it as well, we will have to understand the importance of starting early and the magic of compounding. Albert Einstein said “Compound Interest is the eighth wonder of the world.”

While most of us are aware of this above quote, but we often fail to understand the gravity of it.

To explain simply— In compounded investments, you earn interest on the interest. This boosts the return you can earn. Let’s take a look:

Current Savings Future Value

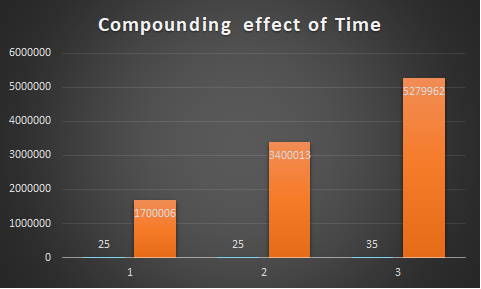

Two friends of same age A & B.

A started early and invested Rs.1,00,000 at the age of 25

B was 10 years late and invested Rs. 1,00,000 aged 35

Both the investment was at 12% compound interest p.a.

At the age of 60.

A earned Rs. 52,79,962 whereas B earned Rs. 17,00,006.

Just 10 years of gap resulted in such a huge gap in returns.

Even if B invested double the amount of A (i.e. Rs.2,00,000), 10 years later.

The amount earned would be Rs. 34,00,013 which is again significantly less than Rs. 52,79,962.

How much should you save each month for achieving Financial Goals ?

Saving Goal

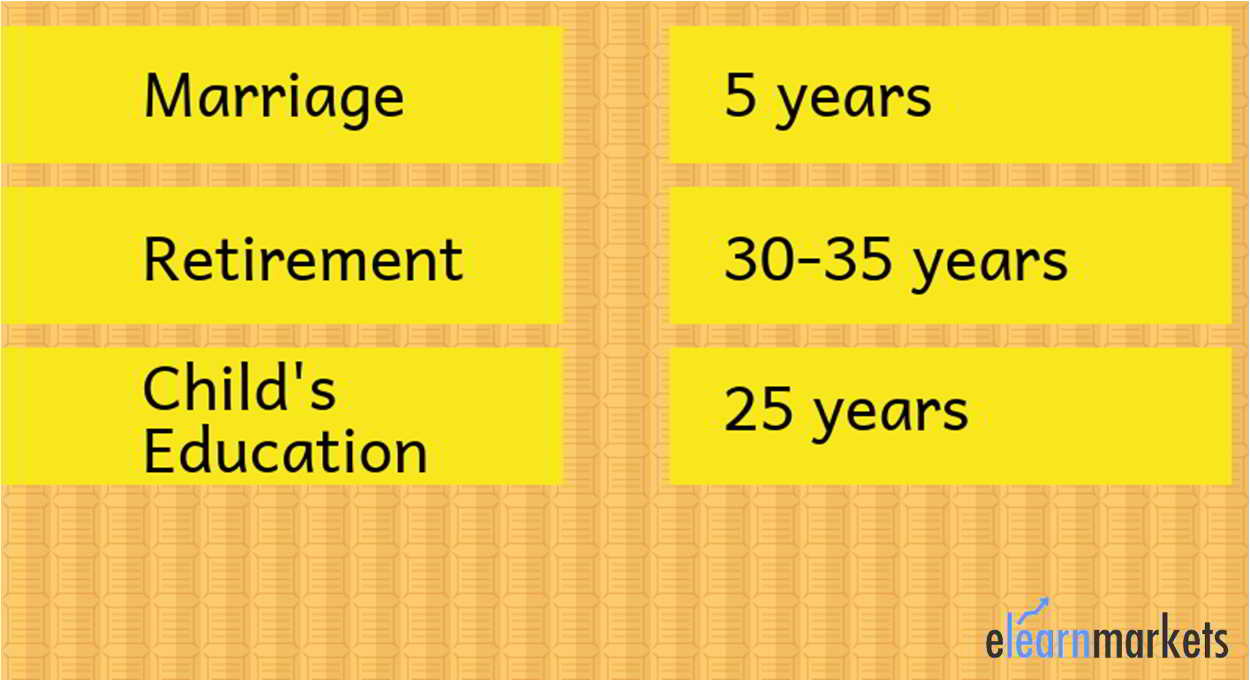

There are financial needs in different stages of our lives. These needs can be classified as Core needs and Aspirational needs.

Number of years

For every financial goal, there is a time frame to achieve it. Say for a 25-year-old:

Other goals will vary as per individual. But the above goals will be more or less on the same timelines.

Achieve your Financial Goals with Financial Planning Made Easy course by Market Experts

How to calculate?

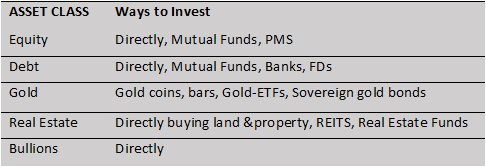

Depending on goals there will be an amount for each goal. Our target is to reach that amount through appropriate investment vehicle. There are several investment vehicles, among them prominent ones are equity, debt, other assets like gold, real estate,etc. These asset classes have their own risks and rewards. One should choose their asset class as per their risk profile but at the same time keep their goals in mind.

Where to put your money?

There are several asset classes to choose from:

Tips for Financial Goals

- Different asset category provides different returns and risks. Equities in general over a long period of time provides better returns than debt. But there are economic cycles where equities do not provide higher return than debt. So, knowing little bit about the economy helps in choosing asset class. Debt investment is preferred if the duration of investment is not long (say under 3 years).

- One of the fundamental purposes of investment is beating inflation. Inflation is the rise in prices of goods and commodities over time. A 1000 rupees will buy lesser quantity of goods one year from today because of inflation.

- Another aspect to take care of would be diversification. Now, why diversification right? Well putting all your money in one particular asset class or fund is risky because if that investment fails, there would be nothing to back you up. So, diversification will help minimize this aspect of risk.But don’t just diversify just for the sake of diversification, choose your asset class wisely.

- Insurance and investments are two different things. A lot of people believe that putting money (premiums) in an insurance scheme is an investment. Do notice that insurance products offer very low returns, if at all. For insurance, a term insurance is always preferable.

- To make a financial plan, first we need to take stock of our cash inflows in the form of salary, business income, etc. and outflows in the form of household expenses, tuition fees, etc. Then we need to set goals and plan accordingly.

Envelope Method

Making budgets is a way to control expenses. One of the popular ways of maintaining budget is “Envelope Method”.

In this method, we divide our expenses into different categories of monthly expenditure. Some common categories could be: groceries, clothing, dining out, entertainment, gas, etc.

Make separate envelopes for each category and put budgeted cash in them. While spending, take out cash from that particular envelope. This way, you can prevent over-spending for a particular category and control expenses.

Source: thebudgetmom.com

Automatic Savings Account

Investments should be done in a disciplined manner. To inculcate this discipline “Automatic Savings Account” is useful. In this account a prior arrangement is made by which a fixed amount is deposited in our investment account automatically at specified intervals.

Savings Shortfall

Monitoring our investment is an important activity that many of us neglect. Say, you have invested with a financial goal in mind and expect a certain rate of return on your investment to reach that goal, right? But, if the returns are not in sync with your goals, you need to look for other options.To make effective financial planning for obtaining your financial goals, you can take assistance of Kredent Money App.

Bottomline

Financial Planning is the key to live a financially secure life.

“Failing to plan is planning to fail “

This cannot be emphasized enough when it comes to financial planning. So, starting today plan prudently to take control of your finances!

{kind=link}