Targeting particular underlying drivers, or factors, that have historically influenced the performance of asset classes or securities is the goal of factor investing. Factor investing aims to capture the excess returns associated with specific traits or variables that have been uncovered through empirical study rather than concentrating only on asset allocation or individual securities selection.

Investors are always looking for ways to control risk and maximize returns in the dynamic world of finance. Factor investing presents a strong substitute for traditional approaches, which frequently concentrate on picking certain stocks or actively participating in the market.

In this blog, we will discuss the fundamental ideas, possible advantages, and considerations of factor investing. We’ll explain how this method goes beyond ordinary market fluctuations by pinpointing particular elements that have historically influenced returns in a range of asset types.

What is Factor Investing?

Choosing particular equities or keeping an eye on the whole market in a passive manner are common practices in traditional investing. A separate strategy is used in factor investing, which looks for and capitalizes on particular elements that have historically driven returns across a range of asset classes.

In essence, factor investing-

- Beyond individual companies: It examines general market factors that impact entire asset classes rather than concentrating on the performance of individual equities.

- Determines the main drivers: These variables may be macroeconomic (such as inflation, interest rates, and economic growth) or quantitative (such as value, size, momentum, and quality).

- Seeks consistent returns: The objective is to outperform the market in terms of risk-adjusted returns by allocating a portion of your portfolio to these factors.

What are the Types of Factors?

Here are the Types of Factors in Factor Investing

Traditional Factors

For many years, factor investing strategies have included these factors, which have been the subject of much study. They are as follows:

1. Value

Value investing involves purchasing stocks that, according to conventional measures such as price-to-book or price-to-earnings ratio, seem to be cheap. The reasoning behind this is that since the market price does not accurately reflect these equities’ fundamental value, there is room for future price appreciation.

2. Size

Concentrates on small- and mid-cap equities, or companies with lower market capitalizations. In the past, these stocks have shown more room for growth than large-cap stocks, but because of their smaller size and possible lack of liquidity, they also come with a larger risk.

3. Momentum

Momentum investing refers to the purchase of equities that have seen notable price increases recently with the goal of profiting from the continuance of this positive trend. The fundamental premise is that equities with significant momentum might keep outperforming in the near future.

Alternative Factors (Quality, Low Volatility, Yield)

Beyond the conventional factors like value, size, and momentum, there are more aspects to consider in factor investing.

They provide investors with more factors to take into account when building their portfolios and looking for profits. Here are some details about three important substitute factors:

Quality

Quality is a company’s stability and sound financial standing. Robust cash flows, low debt levels, steady earnings, and strong fundamentals are characteristics of high-quality companies. Quality-based factor investing looks for and invests in businesses that have strong financial performance and are resilient to market downturns.

These businesses frequently exhibit steady profitability, effective operations, and a competitive edge in their respective markets. Investors seek to minimize downside risk and realize the potential for long-term, sustainable growth by concentrating on quality.

Low Volatility

Choosing stocks or other assets with historically smaller price swings in relation to the overall market is the main strategy behind low volatility investing. Low volatility investing refutes the common knowledge that believes increased risk is always associated with higher returns by highlighting the significance of capital preservation and downside protection.

Low volatility strategies prioritize assets with smoother, less volatile price movements in an effort to provide competitive risk-adjusted returns. Those who want to reduce portfolio volatility and have a more steady investing experience, especially in times of market turbulence, frequently select these kinds of investments.

Yield

Yield-based factor investing focuses on securities that offer attractive income streams, such as dividends or interest payments. Companies or assets with higher yields typically distribute a significant portion of their earnings or cash flows to shareholders, making them appealing to income-oriented investors.

Yield-based strategies may target dividend-paying stocks, high-yield bonds, real estate investment trusts (REITs), or other income-generating assets. While yield investing can provide investors with consistent income streams, it’s essential to assess the sustainability of the yield and the underlying fundamentals of the investments to avoid potential value traps or dividend cuts.

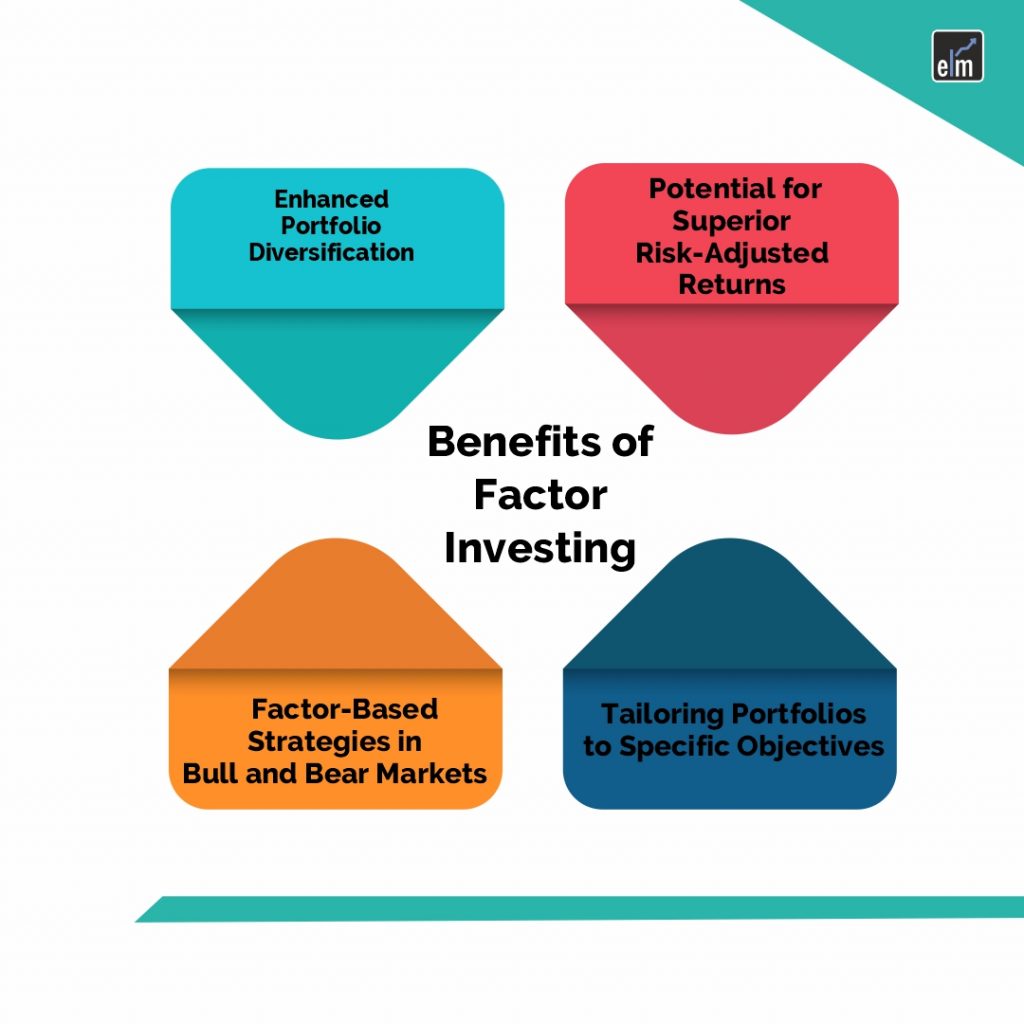

Benefits of Factor Investing

Factor investing has many advantages, including providing investors with a methodical way to manage their portfolios that can increase returns and lower risks. The following are some main advantages:

1. Enhanced Portfolio Diversification

Investors can diversify their portfolios beyond conventional asset classifications via factor investing.

Through focusing on particular elements like value, momentum, or low volatility, investors can uncover revenue streams that might not be highly correlated with overall market fluctuations.

Particularly in times of market instability, this diversity can assist in lowering portfolio volatility and improve risk-adjusted returns.

2. Potential for Superior Risk-Adjusted Returns

The goal of factor investing is to profit from the risk premiums attached to particular factors that have outperformed the overall market over extended periods of time in the past.

Investors may be able to attain superior returns by methodically skewed portfolios in the direction of these factors as opposed to conventional market-cap-weighted techniques.

In addition, factor investing prioritizes risk-adjusted returns with the goal of achieving competitive performance with efficient downside risk management.

3. Factor-Based Strategies in Bull and Bear Markets

Factor-based approaches have proven to be resilient in a variety of market conditions, including bull and bear markets.

Quality and low volatility are two examples of attributes that may have defensive qualities that might support portfolios in times of market turbulence.

On the other hand, momentum-related elements could profit from rising trends in bull markets. Through the integration of many elements in a portfolio, investors can construct resilient investment plans that adjust to fluctuating market circumstances and yield steady returns over an extended period.

4. Tailoring Portfolios to Specific Objectives

Investors can customize their portfolios to meet their unique investment goals, risk tolerances, and preferences via factor investing.

Depending on their financial objectives and limits, investors can tailor factor-based strategies to achieve income, capital appreciation, or downside protection.

Environmental, social, and governance (ESG) factors can also be integrated with factor investing, allowing investors to pursue competitive returns and include sustainability principles into their investment decisions.

Risks Associated with Factor Investing

Although factor investing has many advantages, it also has some risks and difficulties. Investors must be aware of these risks in order to efficiently manage their portfolios and make well-informed decisions. The following are some major dangers connected to factor investing:

Factor Concentration Risks

If a factor is significantly weighted in a portfolio, factor investing methodologies may result in concentration hazards. An excessive dependence on one or a small group of elements may make a portfolio more susceptible to unfavorable market circumstances or unforeseen occurrences. In order to reduce the risk of concentration and improve portfolio resilience, diversification across a number of parameters is crucial.

Model and Data Risk

The identification and exploitation of factor premia in factor investing is based on quantitative models and historical data. Nevertheless, decisions about investments may be compromised by biases, limits, or mistakes in these models and data sources.

The possibility of model mistakes or presumptions that do not fairly represent the dynamics of actual markets gives rise to model risk. Data risk is related to the accuracy, consistency, and dependability of the historical data that factor analysis uses. In order to reduce the risks associated with models and data, investors need to be cautious and perform extensive due diligence.

Market Environment Sensitivity

Factor performance is subject to considerable variation depending on the market conditions, economic cycles, and geopolitical developments. In one state of the market, factors that perform well could underperform or show more volatility in another.

Sensitivity to the market environment might make it difficult for investors to predict factor performance and modify their portfolios appropriately. Market environment sensitivity can have an impact on factor investing techniques, but it can be lessened by active monitoring, adaptability, and diversification across complementary factors.

Overfitting and Backtesting Pitfalls

When investing methods are excessively optimized or customized to historical data, it is known as overfitting, and the outcome is subpar performance in real-world scenarios. Although backtesting is useful for assessing the efficacy of strategies, if it is not done carefully, it may create biases and errors.

Investors developing and validating factor-based models need to be disciplined and aware of the overfitting risk. Sensitivity analysis, out-of-sample validation, and robust testing techniques can all assist in reducing the risks associated with backtesting and overfitting.

Case Study: Constructing a Factor-based Portfolio

We will describe the steps involved in building a factor-based portfolio utilizing value, momentum, and quality in this case study.

1. Factor Selection

The first stage is to determine which factors fit the investor’s risk tolerance and investment goals. Value, momentum, and quality have been selected as the main characteristics in this instance due to their track record of success and advantages in terms of diversification.

2. Data Analysis

To find securities that display traits connected to each component, we then carry out in-depth investigation and data analysis. We look for stocks with low price-to-book ratios, low price-to-earnings ratios, and high dividend yields in order to satisfy the value criterion.

We find equities with strong price performance over a given time period in order to determine momentum. Companies with steady earnings, solid balance sheets, and excellent returns on equity are what we consider to be of good quality.

3.Portfolio Construction

We assign weights to specific stocks or assets under each factor category after choosing securities based on each criterion. In order to lower the risk of concentration and improve portfolio stability, we want to diversify across markets, sectors, and industries.

4. Risk management

To reduce potential negative risks, we take risk management strategies into account during the portfolio construction process. This could entail implementing stop-loss orders, limiting risk, or hedging with derivatives.

5. Monitoring and Rebalancing

After the portfolio is put together, we keep an eye on performance indicators and factor exposures to make sure the investments are in line with our goals. Periodic rebalancing is carried out to take into account shifts in factor dynamics and realign portfolio weights with target allocations.

6. Evaluation of Performance

Lastly, we assess how well the factor-based portfolio has performed in comparison to pertinent benchmarks and investment goals. We evaluate drawdowns, volatility, risk-adjusted returns, and other performance measures in order to determine how successful the factor investing technique is.

Conclusion

Factor investing is a strategy that goes beyond traditional asset class allocations by focusing on specific investment drivers, such as value, momentum, quality, size, and low volatility. By systematically identifying these factors, investors aim to enhance portfolio diversification, improve risk-adjusted returns, and align investments with personal financial goals.

Want to dive deeper into investing? Check out our Beginner’s Guide to Investing to get started!

Frequently Asked Questions (FAQs)

1. What is factor investing?

Targeting particular underlying drivers, or factors, that have historically influenced the performance of asset classes or securities, is the goal of factor investing.

2. What are some common factors in factor investing?

Value, momentum, size, quality, low volatility, and yield are common factors.

3. How does factor investing differ from traditional investing?

Traditionally, assets are distributed throughout a variety of asset classes, such as stocks, bonds, and real estate. In contrast, factor investing places emphasis on leveraging particular characteristics within various asset classes in order to generate profits.

{kind=link}