Bank’s purpose is to provide loans to businesses. This creates credit in the economy. But, with credit comes the risk of credit default. Have you heard about Banking NPA?

Loans or advances provided by the banks are considered as banks’ assets as banks will earn interest on them. The businesses sometimes default on the loan repayments and this causes banking NPA (non-performing assets).

| Table of Contents |

|---|

| Banking NPA Data |

| Causes for Banking NPA |

| Banking NPA Solution & Role of RBI |

| Other Financial Sector Misery |

| Bottomline |

Credit default by the borrowers is detrimental to the bank’s financial condition. Learning about Credit Risk and Credit Derivatives will help you in understanding credit default.

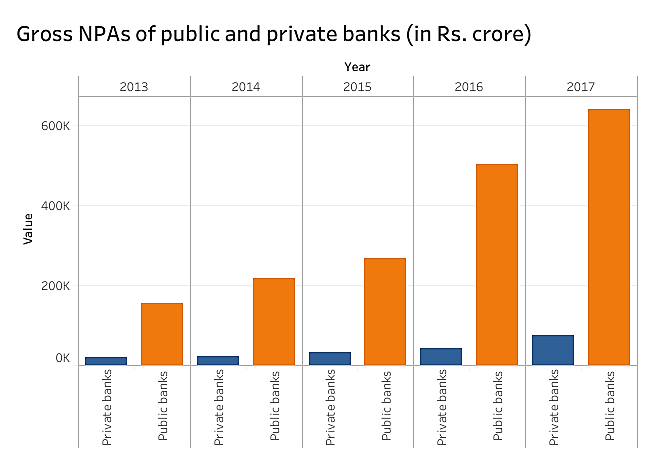

Banking NPA Data –

Indian banks together reported gross non-performing assets (NPAs) of more than Rs. 10.25 lakh crore as of March 2018. 21 PSU Banks alone contributed more than Rs. 8.97 lakh crore out of the total bad loan. Gross NPAs rose to 10.14 percent in March 2018.

Learn how to invest in Share Market with Rs 5000 for Free by Market Experts

The PSU banks’ GNPA ratio was at 13.41 percent of the total advances. After making provisions, the Net NPA stood at Rs. 5.18 lakh crore. Public sector banks led by SBI are in a more precarious situation compared to the private sector banks.

Source: www.thehindu.com

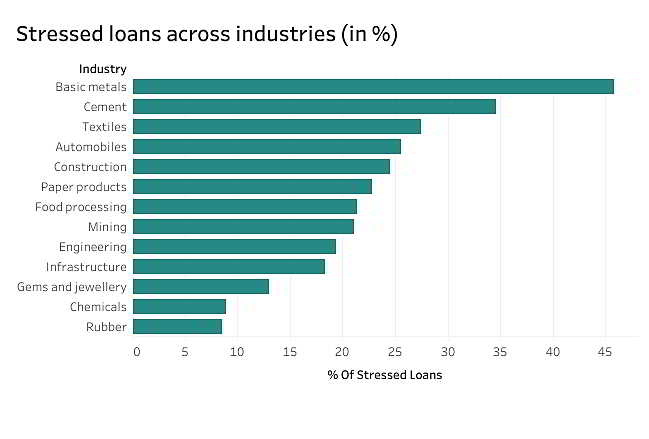

Causes for Banking NPA

Irrational lending and deficiencies in evaluation and monitoring are among the factors that have resulted in Indian banks making bad loans worse.

Sick Industry growth made Banking NPA Rise

- Before the financial crisis of 2008 India’s economy was in a boom phase. During this period banks lent extensively to corporates in the expectation that the good times will continue in future. But future does not always play out as it had been in the past. The businesses of most of the corporates were adversely affected due to slowdown in the global economy following the financial crisis.

- The ban in mining projects, and delay in environmental related permits affected power, iron and steel sector with added volatility in prices of raw material. All these factors weighed heavily on the earning of the corporates. Low earnings affected their ability to pay back loans. This is the one of the most important reason behind increase in NPA of public sector banks.

- Another major reason of rising NPA was the relaxed lending norms for corporate houses.Their financial status and credit rating were not analysed properly. The banks were willing to accept higher leverage and less promoter equity. They even accepted reports by the promoter’s investment banks rather than doing their own analysis. Around 40% of the outstanding loans have been made to companies with interest coverage ratio less than one.Also, to stay competitive, banks were selling unsecured loans which contributed to the high levels of NPAs.

- Public Sector banks provide major portion of the credit to industries and it is this part of the credit distribution that forms a great portion of NPA. In the case of kingfisher airlines financial crisis, SBI provided a huge amount of loan which it is not able to recover from it.

- The priority sector lending (PSL) sector has contributed substantially to the NPAs. Priority sector includes agriculture, education, housing, MSMEs. As per the estimates by the SBI, education loans constitute 20% of its NPAs.

- There are also cases of credit default by promoters, where the funds have been diverted by over-invoicing imports, sourced via, a promoter owned subsidiary abroad or exporting to shell companies and then declaring, that they defaulted.

Source: www.thehindu.com

Banking NPA Solution & Role of RBI

GoI is struggling to come up with solutions thus it set up inter-creditor agreements to speed up resolution under the Insolvency and Bankruptcy Code (IBC). It proposed a combination of a bank-led asset management company, alternate investment funds, and a platform to auction bad assets. To comprehend the scenario, as per estimate, there are nearly Rs 12 lakh crore of stressed assets in the country’s banking system.

The stressed asset constitutes 15 percent of the outstanding loan books of these banks. Banks have sold around Rs 2 lakh crore worth of such loans to asset reconstruction companies (ARCs), leaving about Rs 10 lakh crore on their own books. In such a scenario, the RBI direction on referring companies to the National Companies Law Tribunal (NCLT) could help tackle the NPA menace to a great extent. While the action plan details are being worked out, the process has already been initiated for a few cases.

As per the estimates, more than 70 percent of these cases will be restructuring and resolutions wherein the debt will be written down to sustainable levels. It is estimated that around Rs 40,000-50,000 crore of additional capital will have to be infused to make these companies perform efficiently again. This will be infused by a mix of existing promoters, ARCs, stressed asset funds, and private equity (PE) investors. These investors will also drive the turnaround for these companies through stronger management.

Other Financial Sector Misery

Brexit impact on Banking

- Brexit is the event of Britain leaving the European Union. The British citizens voted to exit the European Union. This is a major event because earlier Indian companies had headquarters in UK and from there; they conducted business throughout Europe under the free European market system.

- New trade deals with European countries will have to be forged by the Indian companies and government. The Indian financial sector which has exposure to the Indian companies and other foreign companies in Britain would be affected accordingly.

- Due to its economic size and growth rate, India attracts huge foreign investment and after Brexit both Britain and Europe would want a major portion of that pie. On the other hand, India is the third largest investor in Britain. So, UK would also try to maintain stronger ties with India.

- As a result of Brexit, UK might not be as suitable to do business as before. The Indian companies will have to set up base in other European nations as well. However, Britain would not want to lose out on Indian investment and may attract Indian companies by offering favourable trade agreement.

- India has a trade surplus of $3.64 billion with Britain.

GST Impact on Banking NPA

- GST has been a landmark indirect tax reform in India. It tried to make India a unified business zone rather than divided by states which had a lot of complications.

- NBFC and Banks with pan-India presence until now could discharge their service tax compliance through single centralized registration. However, under GST they have to obtain separate registration for every state they operate in. Compliance burden has also increased in terms of periodicity and number of returns.

- Banks and NBFCs mostly opt for the option of reversal of 50% of the CENVAT credit availed against inputs and input services. Under GST, 50% of the CENVAT credit availed against inputs, input services, and capital goods will have to be reversed which leaves them with a position of reduced credit of 50% on capital goods thus increasing cost of capital.

- IT systems will need to be adapted to serve the purpose of solving the complexity related to GST compliance and procedures at a higher volume.

- The impact of GST on Banks and NBFCs will be such that operations, transactions, accounting and compliance will need to be reconsidered entirely.

Payment Banks impact on the Indian banking system.

- The payment banks will increase competition in banking industry. In an already crowded banking industry, the introduction of new players from different sectors setting up these payment banks bringing their own marketing ideas and different customers on board will steepen the battle for customers. Also, with more competition, the services and products is expected to get better thus increasing competition for the Banks.

- Consumers would be free to open both savings bank accounts and current bank accounts with payment banks. Payment banks will attract both retail as well as business customers. Consider the India Post Payments Bank. The bank will charge a nominal fee of up to Rs. 35 for this. This facility will be available for transactions that are less than Rs. 10,000. Such facilities will help financial inclusion to a great extent.

- Workers living in cities and away from their rural homes will be able to send money directly through payments banks. These payments banks are expected to be easily accessible by their immediate family members when compared to commercial banks.

- Payments banks have the ability to change the face of rural India in near future. But don’t forget to compare financial products across banks before you select one.

Watch this video to know about the important banking terms –

Bottomline

A strong banking sector is a necessity for a flourishing Industry. The failure of the banking sector will have an adverse impact on other sectors of the Industry. By providing lending services, banks create credit in the economy. One person’s spending is another person’s earning.

More the credit in a society, more the economic activities in the Industry. Therefore, credit helps an economy prosper. Banks and other financial institutions do the job of creating credit and boosting economic activities in the industry. In other words, we can say, the banking industry is the backbone of any economy.

Don’t forget to share your view!!

Visit Stockedge to avail latest stock market updates at ur fingertips.

{kind=link}