Traders that own the underlying asset and are bullish on it over the long run adopt the synthetic call strategy. However, he is equally concerned about potential negative outcomes. With no risk, this tactic offers limitless return potential.

Using this method, you purchase Put options on the long-term holding underlying. You gain from assets if the price of the underlying increases. If it does, your loss will be limited to the put option premium you paid.

What is Synthetic Call Options Strategy?

Investors and traders that utilise the synthetic long call strategy buy a stock because they have an optimistic outlook on it. But what if the stock price falls instead? As an investor, you wish you had some protection from a price decline.

Thus, purchase a Put on the stock. As a result, you have the option to sell the shares at the strike price. The strike price can be somewhat above (ATM strike price) or below the price you paid for the shares (OTM strike price).

Not the same as the Buy Call Options Strategy

However, the approach is not to buy call options. With this exposure, you want to hold the underlying stock and profit from price appreciation, dividends, bonus rights, etc. while also protecting yourself from a downward price trend.

In a straightforward purchase of a call option, there is no underlying stock holding; rather, the transaction is made only to profit from price movement in the underlying stock.

How does it work?

Let us discuss how to implement the strip options strategy:

1. Outlook

When a trader is bullish on long-term holdings but also worried about the potential downside risk, they use a synthetic call option strategy.

2. Strategy

Using this method, you purchase Put options on the long-term holding underlying. You gain from assets if the price of the underlying increases. If it does, your loss will be limited to the put option premium you paid.

3. Synthetic Call Example

Let’s say you have a bullish view for TCS, which is now trading at Rs 3,400. However, you are also worried about potential losses should the TCS stock price decline. A synthetic call strategy might be used in this situation by purchasing TCS stock at the current market price. You purchase a Put option with a strike price of Rs 3300 at a premium of Rs 150 to hedge against a decline in TCS’s price.

4. Maximum loss\risk

Losses are limited to Stock price + Put Premium-Put Strike price

5. Profit

The Profit potential is unlimited when this strategy is implemented.

6. Breakeven stock price at expiration

The breakeven point is – Put Strike Price+ Put Premium + Stock Price—Put Strike Price

You can also read our blog on 12 Common Option Trading Strategies Every Trader Should Know

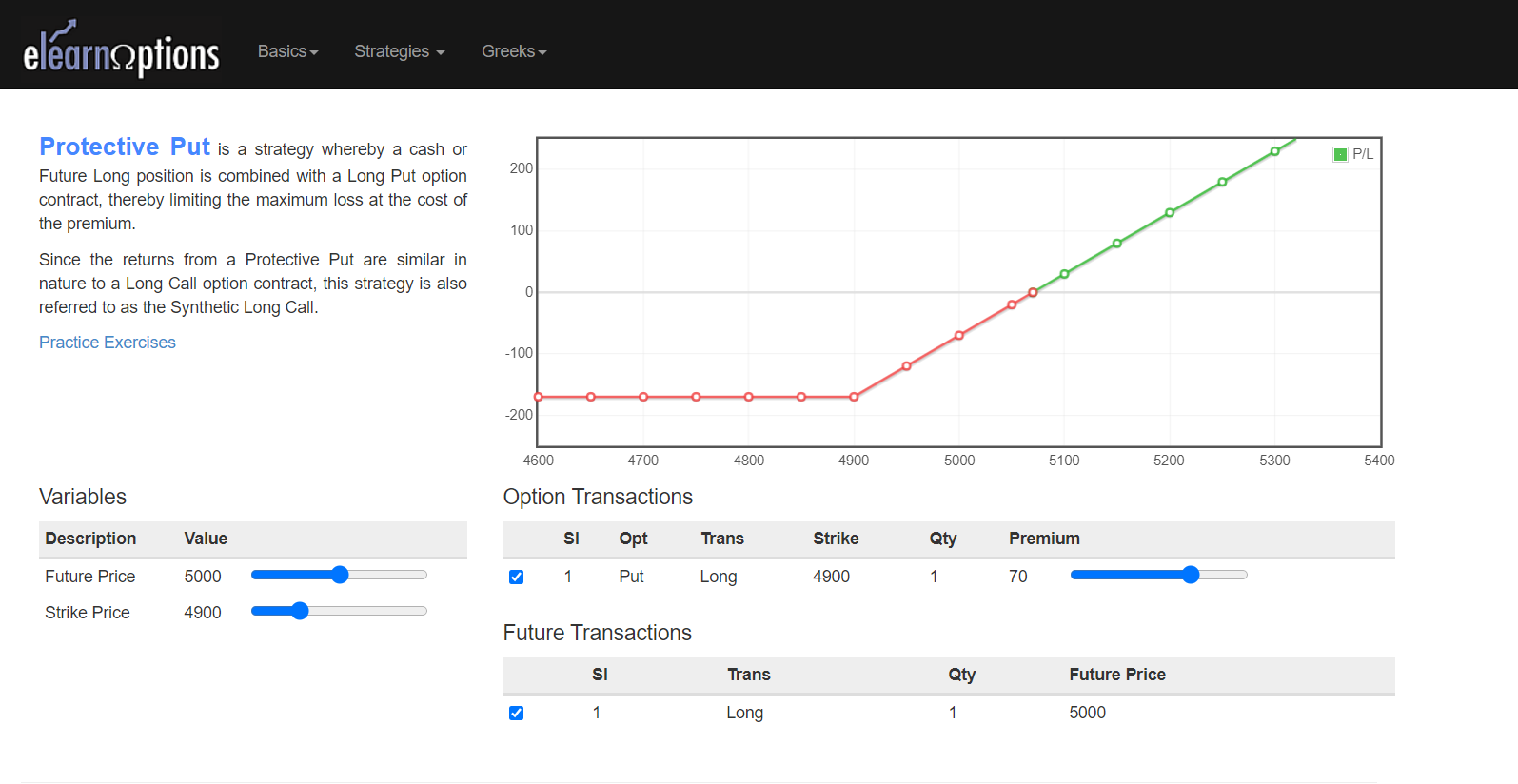

7. Payoff Diagram

Below is the payoff diagram of this strategy

You can practice more such strategies in ElearnOptions

Bottomline

This strategy carries little risk. In the event of a market decline, this method minimises the loss, but when the stock price rises, the potential return is limitless. a sound approach when buying a stock with the intention of protecting any downside risk over the medium or long term. Synthetic Long Call is the name given to the payoff because it resembles the purchase of a call option.

We hope you found this blog informative and use it to its maximum potential in the practical world. Also, show some love by sharing this blog with your family and friends and helping us in our mission of spreading financial literacy.

Happy Investing!

You can also visit web.stockedge.com, a unique platform that is 100% focused on research and analytics.

{kind=link}